Defensive Saving Behavior: Romanians Are Saving for Survival, Not Growth

- futureofromania

- May 31

- 13 min read

Defensive Saving Behavior: Romanians Are Saving for Survival, Not Growth

Emergency-First Mindset: Financial Security Replaces Wealth Building

Saving is no longer about getting ahead

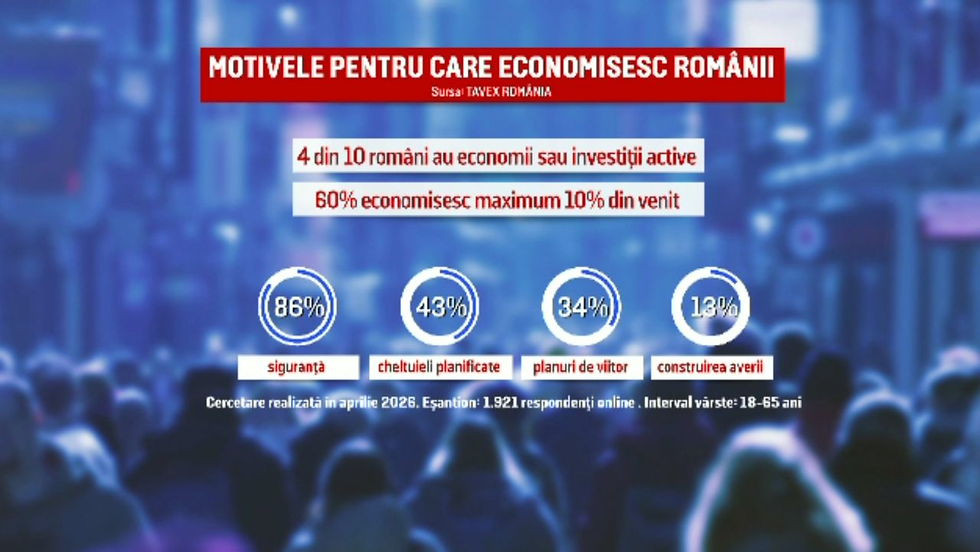

Romanians are not stopping saving—but they are changing why they save. Only 4 in 10 manage to put money aside, and even among them, the overwhelming majority save for emergencies, not for wealth creation. The contradiction is striking: saving behavior exists, but it is defensive, not aspirational.

This signals a deeper cultural shift from growth-oriented financial thinking to risk-avoidance and survival logic. Saving is no longer about building the future—it is about protecting against uncertainty. Emotionally, money becomes a buffer, not a tool for progress.

Trend Overview: Saving behavior shifts from growth to protection

• What is happening: Low saving participation across populationOnly around 40% of Romanians are able to save consistently➡️ Financial resilience remains limited This indicates that saving is not a widespread habit, but rather a constrained behavior dependent on income pressure, making financial stability uneven across the population.

• Why it matters: Savings are small and insufficientMost people save less than 10% of income➡️ Emergency buffers remain weak This creates a fragile system where even those who save are not fully protected, increasing vulnerability to shocks like job loss or unexpected expenses.

• Cultural shift: Saving becomes defensive, not aspirational86% save for emergencies, not investments➡️ Wealth-building mindset declines Instead of focusing on growth, consumers prioritize security and protection, reflecting a broader psychological shift toward caution.

• Consumer relevance: Financial anxiety drives behaviorFear of unexpected events shapes saving decisions➡️ Emotional security becomes key driverSaving is no longer rational-only—it is deeply emotional, tied to fear, uncertainty, and need for control.

• Market implication: Investment culture remains underdevelopedOnly a small share save for wealth growth➡️ Long-term financial markets grow slowlyThis limits capital formation and signals a slow transition toward more sophisticated financial behaviors.

Trend Description: The mechanics of survival-driven saving

• Context: Rising cost of living and income pressureExpenses increase faster than savings capacity➡️ Limits ability to build reserves Consumers operate in a system where saving is constrained by necessity, not choice.

• How it works: Saving as a reactive bufferMoney is set aside primarily for emergencies➡️ Acts as protection, not investmentSavings are treated as a safety net, not a growth engine.

• Key drivers: Uncertainty and lack of financial confidenceConsumers expect instability➡️ Encourages precautionary behaviorThis reinforces a mindset where risk avoidance dominates decision-making.

• Why it spreads: Shared financial vulnerabilityLarge segments face similar constraints➡️ Behavior becomes normalizedSaving for emergencies becomes a collective survival strategy, not an individual preference.

• Where it is seen: Across income levels, but stronger in middle segmentsMiddle-income households struggle to balance expenses and savings➡️ Financial pressure is widespreadThis group experiences the strongest tension between income and cost, driving pragmatic behavior.

• Key Players & Influencers: Banks, financial advisors, and traditional saving toolsSavings accounts, cash holding, basic instruments dominate➡️ Innovation adoption remains slowConsumers stick to simple, low-risk solutions, avoiding complexity.

• Future: Continued dominance of defensive saving behaviorGrowth-oriented saving will remain limited➡️ Financial behavior stabilizes around protectionUnless income conditions improve, saving will remain reactive rather than strategic.

Insight: Saving is being redefined as protection, not progress

This shows that financial behavior is shifting toward defensive saving strategies focused on resilience rather than growth, reflecting a deeper cultural adaptation to uncertainty.

It matters because it limits long-term wealth creation and keeps consumers in a cycle of short-term financial management rather than upward mobility.

Value is shifting toward security, liquidity, and accessibility, rather than return on investment or long-term gain.

Financial institutions must adapt to consumers who prioritize certainty and control over performance and risk-taking.

The deeper transformation reflects a pragmatic, uncertainty-driven economy, where saving is no longer a tool for advancement—but a mechanism for survival and stability.

Why Defensive Saving Is Rising: Income Pressure, Uncertainty, and Pragmatic Financial Behavior Converging

Saving behavior in Romania is no longer driven by long-term ambition—it is driven by short-term survival logic and emotional security needs. Consumers are navigating an environment where future predictability is low, making long-term financial planning feel risky or even unrealistic.

The contradiction is essential: people understand that investing and long-term saving are important, yet their current reality forces them into defensive behavior. This creates a system where financial decisions are guided less by opportunity and more by risk avoidance and stability preservation.

Elements Driving the Trend: Financial pressure reshapes saving logic

• Rising cost of living reduces saving capacityExpenses for essentials leave little room for saving➡️ Limits ability to build reservesAs fixed costs (food, utilities, rent) increase, savings become what is left—if anything—after survival expenses. This turns saving into a residual outcome, not a planned strategy, making it inconsistent and fragile.

• Low income growth and stagnation perceptionIncome does not increase at the same pace as expenses➡️ Reduces long-term financial confidenceConsumers begin to feel that financial progress is out of reach, creating a psychological ceiling where investing or long-term planning feels disconnected from reality.

• High exposure to unexpected expensesFrequent financial shocks (health, repairs, bills)➡️ Encourages emergency-first savingThis reinforces a loop where savings are constantly built and then depleted, preventing accumulation and reinforcing short-term thinking.

• Short financial resilience horizonOnly a minority can sustain themselves beyond a few months➡️ Reinforces survival-oriented mindset Consumers operate in compressed financial timelines, focusing on the next 1–3 months rather than years, which fundamentally limits strategic behavior.

• Low trust in long-term financial planningFuture outcomes perceived as uncertain➡️ Reduces motivation for investmentWhen the future feels unstable, committing money long-term feels risky, pushing consumers toward liquid, reversible decisions.

• Preference for simple saving methodsCash or basic accounts preferred over investments➡️ Limits wealth-building opportunities Simplicity provides psychological comfort, even if it reduces returns. Consumers choose clarity and control over complexity and potential gain.

• Emotional need for control and safetySaving provides psychological reassurance➡️ Reinforces habit even if inefficientEven small savings act as a mental safety net, reducing anxiety and increasing perceived stability, which reinforces the behavior emotionally.

• Cutting discretionary spending to enable savingRestaurants, vacations, and fashion reduced➡️ Reallocates funds toward security This creates a trade-off where experience-based consumption declines, replaced by precautionary financial behavior.

• Limited adoption of advanced financial toolsLow usage of investment platforms or automation➡️ Slows behavioral evolutionWithout tools that simplify investing, consumers remain stuck in basic saving habits, unable to transition toward wealth-building strategies.

• Social normalization of cautious financial behavior“Better safe than sorry” mindset spreads➡️ Reinforces collective prudenceBehavior becomes culturally embedded, making defensive saving the expected norm, not an exception.

Virality of Trend: Financial caution spreads through shared anxiety and behavior

Defensive saving spreads organically through shared narratives of financial pressure. Conversations about rising costs, uncertainty, and instability create a collective mindset where caution is seen as rational and necessary.

Media, peer discussions, and everyday experiences reinforce the idea that saving is not optional—it is essential for survival.➡️ This transforms saving from a personal strategy into a socially reinforced behavioral norm, deeply embedded in culture

Consumer Reception: Saving feels necessary but insufficient

Consumers accept saving as necessary, but emotionally, it does not provide full reassurance. Even those who manage to save feel that their reserves are too small to truly protect them.

This creates a constant psychological tension:

“I’m doing the right thing”

“But it’s probably not enough”

➡️ Saving becomes both a coping mechanism and a source of underlying anxiety, reinforcing cautious behavior

Consumer Description: The Defensive Saver

The modern Romanian consumer evolves into a defensive saver, whose primary goal is not growth but protection. Financial identity shifts from opportunity-seeking to risk-minimizing behavior.

They:

Save inconsistently, depending on available funds

Avoid complexity and unfamiliar financial products

Prefer liquidity over long-term locking of money

➡️ This creates a behavioral model where financial decisions are reactive, controlled, and safety-driven, rather than strategic

Demographics: Financially constrained but behaviorally aligned population

• Age: 25–60 — economically active population navigating financial pressure

• Gender: Balanced distribution, similar concerns across segments

• Geography: Present across both urban and rural areas

• Income: Strongest impact in middle and lower-middle segments

• Profession/life stage: Employees, families, individuals managing household budgets

• Digital behavior: Basic banking usage, low engagement with advanced financial tools

This is a systemic behavioral shift affecting the majority, not a niche segment.

Lifestyle: Controlled, cautious, and stability-oriented living

Consumers are reshaping their lifestyles around risk management and financial discipline. Spending is monitored, unnecessary expenses are reduced, and decisions are made with caution.

Experiences are not eliminated—but they are filtered through a value and necessity lens.This creates a lifestyle defined by control, not expansion—where every decision is evaluated for its impact on stability.

Consumer Motivation: Security, control, and risk minimization

• Build emergency buffer➡️ Protect against unexpected eventsThis reflects a fundamental need for predictability in an unpredictable environment.

• Maintain financial stability➡️ Avoid disruption in daily lifeConsumers prioritize continuity over growth, ensuring they can sustain their current lifestyle.

• Reduce exposure to risk➡️ Preserve existing resourcesRisk avoidance becomes more important than opportunity seeking.

• Retain access to liquidity➡️ Enable fast response to financial shocksLiquidity becomes a core value driver, even over returns.

• Feel in control of financial situation➡️ Reduce stress and uncertaintyControl is not just financial—it is emotional, shaping overall well-being.

Why Trend Is Growing: Uncertainty aligns with pragmatic financial behavior

This trend accelerates because it directly matches both external conditions and internal needs.

• Emotional driver: Fear of instability and desire for safety➡️ Drives consistent defensive behaviorFear becomes a primary decision-making force, shaping long-term habits.

• Industry context: Rising costs and constrained income growth➡️ Limits capacity for investmentStructural economic factors reinforce short-term thinking.

• Audience alignment: Shared financial pressure across population➡️ Behavior becomes normalizedWhen everyone behaves cautiously, caution becomes the standard.

• Motivation alignment: Control over growth➡️ Reinforces pragmatic mindsetConsumers choose certainty over ambition, redefining success.

Insight: Saving behavior is shifting from wealth-building to survival management

Consumers are transitioning toward defensive, short-term saving strategies, prioritizing stability over growth. This reflects a structural adaptation to economic pressure rather than a temporary behavioral shift.

This matters because it limits wealth accumulation and upward mobility, keeping consumers in a cycle of financial maintenance rather than expansion.

Value is shifting toward liquidity, accessibility, and emotional reassurance, where feeling safe becomes more important than achieving returns.

Financial institutions must adapt by offering solutions that combine simplicity, transparency, and low perceived risk, aligning with current consumer psychology.

The deeper transformation reflects a pragmatic, uncertainty-driven society, where saving becomes a tool for control and protection—mirroring broader shifts in consumption, healthcare, and lifestyle behavior toward cautious, adaptive decision-making.

Trends 2026: Defensive Finance and Stability-First Behavior Reshaping Economic Participation

By 2026, Romania will operate within a defensive financial ecosystem, where most consumers are not optimizing for growth, but for resilience and survival. Financial decisions will be filtered through a strict lens: “Will this protect me if something goes wrong?”

This creates a structural transformation in the economy: demand does not disappear, but it becomes conditional, delayed, and highly justified. Instead of expanding consumption and investing aggressively, consumers move toward controlled participation, engaging only where risk feels manageable and value is clear.

Trend Elements: Financial behavior becomes protection-driven and short-term focused

• Emergency-first saving dominanceSavings are primarily allocated for unexpected events➡️ Long-term wealth-building is deprioritizedThis shifts financial systems toward short-term liquidity models, reducing capital available for long-term investments and slowing wealth accumulation across the population.

• Low savings accumulation capacityMost consumers save small amounts (<10% income)➡️ Financial buffers remain fragile Even disciplined savers struggle to build meaningful reserves, creating a false sense of security that can collapse under larger financial shocks.

• Short-term financial planning horizonFocus limited to 1–3 months survival➡️ Long-term strategies declineConsumers operate in compressed financial timelines, where decisions are made based on immediate needs rather than future growth opportunities.

• Liquidity prioritization over returnsAccess to money valued more than investment gains➡️ Conservative financial behavior dominatesThis reflects a shift where flexibility and reversibility are more important than maximizing returns.

• Investment avoidance behaviorLow participation in stocks, funds, or complex assets➡️ Wealth inequality risks increaseConsumers who avoid investments miss opportunities for growth, reinforcing a gap between financially active and passive populations.

• Consumption filtering mechanismSpending evaluated through necessity and risk➡️ Discretionary spending declinesEvery purchase must now pass a value justification test, reducing impulsive or aspirational consumption.

• Experience reduction trade-offCutbacks in travel, dining, fashion➡️ Lifestyle becomes more restrained This leads to a cultural shift where experiences are no longer default, but conditional luxuries.

• Financial anxiety persistenceSaving does not fully eliminate stress➡️ Psychological pressure remains highEven with savings, consumers feel exposed, creating a state of continuous low-level financial stress.

• Traditional saving method dominanceCash and simple accounts preferred➡️ Innovation adoption remains limited Financial behavior remains structurally conservative, slowing modernization of personal finance systems.

• Control-driven financial identityConsumers define success as stability➡️ Growth ambition declinesSuccess becomes “not losing ground” rather than “getting ahead”, redefining financial aspiration.

Trend Table: Defensive finance reshaping economic behavior

Trend Name | Description | Strategic Implications |

Emergency Saving Priority | Savings for protection | Demand for liquidity products rises |

Low Savings Capacity | Small reserve levels | Financial fragility persists |

Short-Term Planning | Limited time horizon | Long-term products underperform |

Liquidity Preference | Access over returns | Flexible financial tools win |

Investment Avoidance | Low risk appetite | Wealth gap may widen |

Filtered Consumption | Justified spending | Brands must prove value |

Experience Reduction | Lifestyle trade-offs | Leisure sectors pressured |

Persistent Anxiety | Stress despite saving | Emotional positioning matters |

Traditional Saving | Low innovation adoption | Simplicity becomes key |

Stability Identity | Success = security | Aspirational messaging weakens |

Summary of Trends: Finance becomes a system of protection, not expansion

• Main Trend: Defensive Finance Economy➡️ Consumers prioritize protection, liquidity, and control over growthThis signals a structural shift where financial systems must support resilience rather than ambition.

• Social Trend: Normalized financial caution➡️ Risk avoidance becomes a shared behavioral standardCaution evolves from individual reaction into collective mindset.

• Industry Trend: Demand filtering and delayed spending➡️ Consumers engage selectively and conditionallyBusinesses must adapt to slower, more deliberate decision cycles.

• Main Strategy: Simplified, low-risk financial solutions➡️ Reduce complexity and increase perceived safetySuccess depends on removing barriers and lowering perceived risk.

• Main Consumer Motivation: Stability and control➡️ Financial behavior driven by emotional reassuranceControl becomes the primary value driver, replacing growth.

Cross-Industry Expansion: The Rise of the Pragmatic Stability Economy

This financial behavior reflects a broader macro trend—the rise of a pragmatic stability economy, where individuals prioritize control, predictability, and resilience across all areas of life.

In healthcare, people self-diagnose first. In consumption, they cut discretionary spending. In travel, they plan more cautiously. Across industries, the same pattern emerges: reduce risk, maintain flexibility, protect resources.

This macro shift is not temporary—it is a response to prolonged uncertainty. Consumers are not retreating—they are recalibrating participation, engaging with systems in a more controlled and selective way.

Expansion Factors: Defensive behavior spreading across ecosystems

• Economic uncertainty persistence➡️ Reinforces cautious decision-makingUncertainty becomes a constant, not an exception, shaping long-term behavior.

• Rising cost structures across categories➡️ Reduces disposable incomeConsumers have less flexibility, forcing prioritization.

• Emotional fatigue from financial pressure➡️ Increases need for stabilityChronic stress drives preference for predictable systems.

• Low trust in long-term outcomes➡️ Limits investment behaviorConsumers avoid commitments that feel irreversible.

• Behavioral spillover across categories➡️ Pragmatism extends beyond financeFinancial caution influences lifestyle, health, and consumption.

• Digital transparency of financial strain➡️ Awareness increases anxietyConstant exposure to economic news reinforces cautious behavior.

• Limited financial education adoption➡️ Slows transition to advanced toolsConsumers remain in basic financial patterns.

• Social reinforcement of caution➡️ Shared narratives normalize behaviorCaution becomes culturally accepted and expected.

• Time-based financial decision-making➡️ Short cycles dominate planningConsumers think in months, not years.

• Control-first mindset adoption➡️ Aligns with broader pragmatism trendControl becomes central across all decision-making.

Insight: Financial systems are being restructured around protection, not growth

This shows that the economy is shifting toward a protection-first model, where individuals prioritize resilience over expansion, fundamentally changing how financial systems operate.

It matters because it reduces participation in growth-oriented activities, potentially slowing economic dynamism and long-term wealth creation.

Value is shifting toward liquidity, flexibility, and emotional reassurance, creating demand for simpler, safer financial products.

Businesses and financial institutions must adapt to consumers who prioritize control, predictability, and low risk, redesigning offerings to match these expectations.

The deeper transformation reflects a pragmatic, uncertainty-driven economic model, where individuals optimize for survival and stability—reshaping not only finance, but participation across all consumer systems.

Innovation Opportunities: Turning Defensive Saving Into Structured Financial Stability Systems

The biggest opportunity in this trend is not to push consumers toward investment—but to meet them where they are: in protection mode. Innovation must start by respecting the current mindset—low risk, high control, high liquidity—and then gradually evolve behavior toward smarter financial systems.

At the same time, financial ecosystems must solve a critical gap: consumers want safety, but current tools often require discipline, knowledge, or effort. The next wave of innovation will remove this friction by embedding automatic stability-building mechanisms into everyday financial behavior.

Innovation Directions: Systems that transform defensive saving into scalable financial resilience

• Automated micro-saving systemsSmall amounts saved automatically from daily transactions➡️ Builds reserves without effortThis removes the biggest barrier—behavioral inconsistency—by making saving passive, helping consumers accumulate funds even with limited income.

• Dynamic emergency fund buildersTools that calculate and adjust savings targets in real time➡️ Aligns saving with actual risk exposureInstead of generic advice, these systems create personalized safety thresholds, making saving more relevant and actionable.

• Liquidity-first financial productsSavings accounts with instant access and flexible rules➡️ Matches consumer need for controlProducts must balance accessibility with structure, ensuring users feel safe without locking funds.

• Predictive financial stress alertsAI systems that warn about upcoming financial pressure➡️ Prevents reactive decisionsThis shifts behavior from reactive to semi-proactive, helping consumers anticipate rather than just respond.

• Hybrid saving-investment productsLow-risk tools combining safety with modest growth➡️ Bridges gap between saving and investingThese products act as a transition layer, helping consumers gradually move beyond defensive behavior.

• Behavior-based budgeting ecosystemsApps that adapt to real spending habits➡️ Reduces planning complexityInstead of forcing discipline, systems align with actual behavior, making financial management feel natural and achievable.

• Invisible saving mechanisms in banking appsRound-ups, hidden allocations, automated transfers➡️ Builds savings subconsciouslyThis leverages behavioral design to turn saving into a background process, not a conscious effort.

• Emergency-first financial planning frameworksTools prioritizing resilience before growth➡️ Matches current consumer mindsetThis aligns with reality: consumers need security before ambition, not the other way around.

• Trust-first financial education platformsSimple, practical, non-technical guidance➡️ Encourages gradual behavior evolutionEducation must shift from theory to actionable micro-decisions, helping users build confidence step by step.

• Stability-based financial ecosystemsIntegrated systems combining saving, spending, and planning➡️ Reduces fragmentation and confusionThe goal is to create a single environment of control, where all financial decisions are simplified and connected.

Summary of the Trend: Defensive saving reshapes financial ecosystems

• Trend essenceShift from growth-oriented finance to protection-first behaviorThis reflects a structural move toward resilience-focused financial thinking.

• Key driversEconomic pressure, uncertainty, low income growth, emotional need for controlThese forces create a system where risk avoidance dominates financial decisions.

• Key playersBanks, fintech platforms, savings tools, financial advisory ecosystemsThe landscape becomes more service-oriented and behavior-driven, not just product-driven.

• Validation signalsOnly 4 in 10 save; majority save for emergencies; low financial resilience These indicators confirm that defensive saving is already mainstream behavior.

• Why it mattersRedefines financial participation and limits wealth creationThe system shifts from expansion to maintenance and protection.

• Key success factorsSimplicity, automation, trust, flexibility, emotional reassuranceSolutions must reduce effort and increase perceived safety and control.

• Where it is happeningAcross everyday financial behavior, saving habits, and consumption decisionsThis is embedded in daily life, not isolated financial planning.

• Audience relevanceHighly relevant across middle and lower-middle segmentsThis is the dominant consumer reality, not a niche trend.

• Social impactNormalizes cautious, stability-first financial behaviorFinancial ambition is replaced by financial preservation culture.

Conclusion: Finance shifts from growth ambition to stability optimization

Insights: Financial behavior is evolving into a stability-first system where protection, liquidity, and control dominate decision-making, reshaping how individuals interact with money. Industry Insight: Financial institutions must design for automation, simplicity, and low-risk engagement, aligning with consumers who prioritize safety over performance. Consumer Insight: Consumers are becoming more pragmatic, cautious, and control-oriented, redefining financial success as maintaining stability rather than achieving growth. Social Insight: Defensive saving is becoming a normalized collective behavior, reflecting broader economic anxiety and shared uncertainty. Cultural/Brand Insight: The future belongs to financial ecosystems that enable confidence, clarity, and effortless stability, helping consumers navigate uncertainty without complexity. Final Link: This transformation reflects the broader rise of uncertainty and pragmatism, where individuals redesign their financial lives around resilience and control—optimizing not for expansion, but for sustainable survival and long-term stability.

Comments